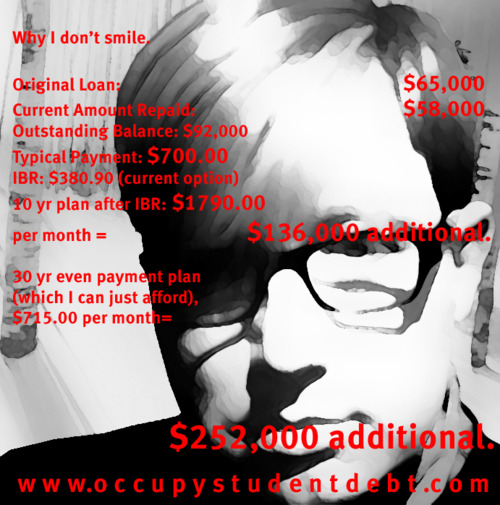

I appreciate your determination to move forward with getting student loan debt forgiven. However after looking into the possibilities for myself I am quite deterred. I want to share a snippet of how I am not helped by Obama’s forgiveness program. I have been teaching in Borough of Manhattan Community College full-time since February 1994. BMCC of the City University of New York is a public sector employer. According to government authorities my employment would qualify for loan forgiveness. I consolidated my numerous student loans amounting to around $96,000 under the Federal Consolidation Loan program with Key Bank (AES Success is the loan manager) in August 2003. It’s now eight years into paying this Federal Consolidation Loan, and I still have a balance of $72,000. To “take advantage” of the forgiveness program recently enacted I would have to apply for a Direct Consolidation Loan and the clock starts again with ten more years of employment in this or another public sector job. To say that I am frustrated is an understatement. Why has there been no “grand-fathering” for people as myself for years spent in repayment of Federal Consolidation Loans?? Were I to apply for a Direct Consolidation Loan I was told I would have to make monthly payments (tied to my income) of over $840. I am currently paying $600 monthly to AES Educational Services. Not much of a bargain and to boot were I to go for the more costly repayment loan and work another ten years (I would be 75 years old at that time!!) I would be forgiven the remaining amount but receive a 1099 form for the amount forgiven and have the “privilege” of paying federal and state taxes on the amount forgiven as income. Is there anything that you can do to make my case/plight known and press for credit for years paid under the Federal Consolidation Loan Program?

Best wishes in our struggle,

Jonathan

Jonathan Lang, PhD, PHD, MPH

Associate Professor, Philosophy and Psychology

Borough of Manhattan Community College of CUNY